|

PureBytes Links

Trading Reference Links

|

Anthony --

After comparing your attached results with my running of your code, I

have a few observations to make.

1. At first, I was thrown off by the entry and exit dates being the

same in backtesting. However, now I understand and accept that.

2. You must have checked,

"Allow same bar exit" in

settings.

3. MOST

IMPORTANT, your code produces very accurate trades, MOST of the time.

However, I noticed what appear to be arithmetic errors on BOTH your

attachment and my backtesting. From the first 10 trades, 8/1/07 -

8/13/07, three trades dated, 8/9/07, 8/13/07, and 8/14/07 are

problematic. The tables below show the problems. The labels

'Anthony', 'Adj', 'Keith', and 'UnAdj' refer to, respectively, your

test results, Yahoo adjusted prices, my test results, and Yahoo

unadjusted prices. My QP3 data base has prices identical to Yahoo

unadjusted, at least for the tables below.

Previous

8/9/07 Close Open High Low Close

Anthony 19.6375 19.208

Adjust 19.71 19.21* 19.64* 18.46* 18.84

Keith 19.70 19.27

UnAdj 19.77 19.27 19.70 18.52 18.90

8/13/07

Anthony 18.8119

18.9216

Adjust 18.79 18.92* 19.82* 18.81* 19.43

Keith 18.87 18.98

UnAdj 18.85 18.98 19.89 18.87 19.49

8/14/07

Anthony 19.418

19.3482

Adjust 19.43 19.35* 19.42* 18.61* 18.66

Keith 19.47 19.40

UnAdj 19.49 19.40 19.47 18.66 18.71

* indicates calculated adjusted values, using simple subtraction.

underlined Prev. Closes should each match the values immediately

below.

instead they match values underlined in other columns.

I did not check any values after the first ten trades.

4. I also tried the following

code below:

SetTradeDelays(0,0,0,0);

Buy = 1;

BuyPrice

= Close;

Sell =

Buy;

SellPrice = Ref(Open, 1);

Short

= Cover

= False;

// long only strategy

It also produces weird results.

However the mismatches are in the Open column rather than in the Prev.

Close column.

-- Keith

Anthony Faragasso wrote:

Keith,

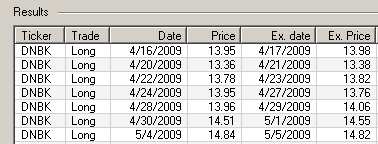

Here is a screen shot of my

results....it produces every day...

I selected current stock and ticker

is Sprint

with a from to range as depicted in

the screen shot

Anthony

----- Original Message -----

Sent:

Saturday, January 30, 2010 12:54 PM

Subject:

Re: [amibroker] Simple Buy on Close, Sell on Open not as expected

Anthony --

Thanks for your effort. I tried your exact code (copy and paste). It

still skips every other day.

Also, I reduced the code to absolute minimum as:

Buy = 1;

BuyPrice = Close;

Sell

= Ref(Buy, -1);

SellPrice = Open;

Been through my settings many times. Still the same.

BTW, I'm running 5.26beta.

-- Keith

Anthony Faragasso wrote:

Keith

give this a try:

Settings window:

allow same bar exit is enabled

all stops are disabled

In the trades window of the

settings I set up the trades as follows probably do not need it :

buy=close, delay 0;sell=open,

delay 0

short=close, delay 0 ,cover =

open, delay 0

// BuyClose SellOpen Daily.afl

SetTradeDelays(0,0,0,0);

Buy = Ref(Close,-1);

BuyPrice = ValueWhen(Buy,Ref(C,-1));

Sell = Open;

SellPrice = Open;

Short = Cover = False;

// long only strategy

-----

Original Message -----

Sent:

Saturday, January 30, 2010 1:09 AM

Subject:

[amibroker] Simple Buy on Close, Sell on Open not as expected

Just fooling around with a very simple idea, but can't get

the code to work.

The idea is to sell at close of every day, hold over night, and sell at

open the following day.

Code below sorta works, but skips every other day. For example:

Day 1, buy on close; Day2, sell on open.

Day 3, buy on close; Day4, sell on open.

etc.

But I can't make it buy on close of days 2, 4, etc.

Tried "Allow same bar exit" in settings, but that makes it sell the

same day that it buys, which is wrong.

// BuyClose SellOpen Daily.afl

SetTradeDelays(0,1,0,0); // has no effect

Buy = Close;

BuyPrice = Close;

Sell = Open;

SellPrice = Open;

Short = Cover = False; // long only strategy

Buy = ExRem(Buy, Sell); // has no effect

Sell = ExRem(Sell, Buy); // has no effect

Well?

-- Keith

|

|